How Payments Work

A payment transaction is the result of multiple systems interacting in real time. While this process is abstracted for both merchants and customers, it follows a clearly defined sequence.

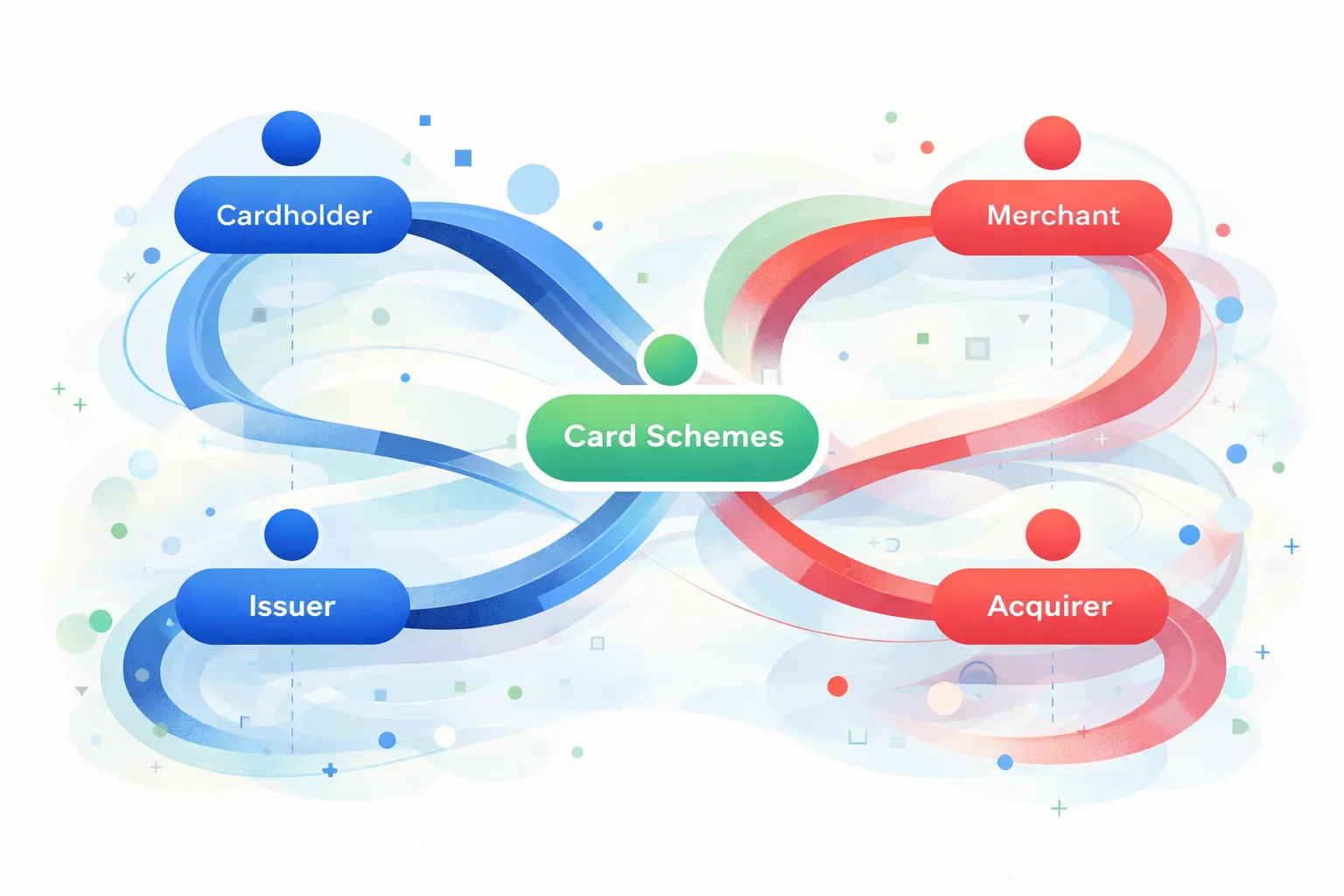

When a customer initiates a payment at a terminal, the device captures the required payment data and sends an authorization request. This request is routed through the acquiring infrastructure, reaches the relevant card scheme, and is forwarded to the issuing bank.

The issuing bank evaluates the request based on factors such as available funds, fraud checks, and card validity. Within seconds, it returns an approval or decline. This response travels back through the same chain and is displayed on the terminal.

If the transaction is approved, it is stored and later included in a settlement process. Settlement is the financial closing of the transaction: the approved payments are finalized in the acquiring systems and the funds are prepared for transfer to the merchant.

In Switzerland, this flow is governed by the EP2 standard. EP2 defines how terminals behave, how transactions are structured, and how communication occurs between terminals and acquiring systems. This ensures interoperability across different terminal providers and a stable payment environment for merchants.

It is important to distinguish between two phases of a transaction:

- Authorization: the real-time approval or decline of a payment

- Settlement: the financial closing and funding step that follows authorization

Understanding this distinction explains why payments appear immediate, while payouts follow a defined schedule.

For a deeper and structured explanation of global payment flows, including all participants and message exchanges, ThePaymentBible is a highly recommended reference.